Appian

Appian builds enterprise software that automates business processes.

Their platform helps large organizations take work that normally lives across emails, spreadsheets, legacy systems and manual approvals and turn it into structured, automated workflows that can be tracked and scaled.

This is not consumer* software and not SMB focused. Appian is built for complex, regulated, high volume environments where speed, compliance and visibility matter.

If I had to explain it simply:

Appian helps big organizations get work done faster with fewer people and fewer mistakes.

What the platform actually includes

Appian is sold as a single integrated platform, not point tools.

Let’s companies build internal apps quickly without large engineering teams

Used for dashboards, intake forms, approval systems and operational tools

Designed so business teams and IT can work together instead of everything bottlenecking with developers

Workflow and case management

Orchestrates multi step processes across teams and systems

Common use cases include claims processing, onboarding, procurement, compliance reviews, investigations, and customer service

Tracks who did what, when and why which matters in regulated industries

Automation and integrations

Connects to existing systems like ERP, CRM, databases, and third party apps

Automates repetitive tasks and handoffs

Often used to modernize workflows without ripping out legacy systems

Data fabric and process intelligence

Pulls data from multiple sources into a single logical view

Lets users analyze how processes actually run vs. how leadership thinks they run

Identifies bottlenecks, delays, reworkand inefficiencies

AI and process mining

Uses machine learning and generative AI to surface insights

Helps companies identify where automation will have the biggest impact

This is positioned as augmentation not replacement of human decision making

Who uses Appian

Customers are almost entirely large enterprises and government agencies.

They explicitly focus on organizations with:

Thousands of employees

Complex internal processes

Heavy compliance or audit requirements

Key verticals

Government and defense

Financial services

Insurance

Life sciences and healthcare

Manufacturing

Energy

Telecommunications

Government exposure

Government is a major part of Appian’s business.

They sell heavily into:

US federal agencies

State and local governments

Defense and national security organizations

This brings:

Long sales cycles

Sticky contracts once deployed

Sensitivity to budgets, shutdowns, and procurement timing

They operate a dedicated government cloud environment designed to meet strict security standards.

How Appian makes money

Appian has 2 revenue streams.

Subscription revenue

This is the core of the business.

Customers pay recurring fees to use the platform

Pricing is typically per user or per application

Subscriptions are often multi year and billed in advance

Cloud subscriptions are the fastest growing portion

This is high margin software revenue and what investors focus on most.

Professional services

Implementation

Custom application development

Training and onboarding

Partnerships and ecosystem

Appian relies heavily on global systems integrators to sell and deploy at scale.

Major partners include:

Accenture

Deloitte

PwC

EY

KPMG

Capgemini

Tata Consultancy Services

These firms:

Bring Appian into large enterprise deals

Handle complex implementations

Expand Appian’s reach without Appian hiring massive services teams

The partner ecosystem is critical. When partners are engaged, deal sizes and stickiness tend to increase.

Competitive landscape

Appian sits in a crowded but fragmented space.

Who they compete with

Other low code platforms

Legacy BPM vendors

Large enterprise software suites that offer workflow tools

Internal custom development teams

Why customers choose Appian

Strong end to end process focus

Deep workflow and case management capabilities

Ability to modernize without replacing core systems

Strong reputation in government and regulated industries

Where competition can be tough

Price sensitivity in commercial enterprise

Large vendors bundling workflow into broader suites

Customers choosing internal builds for simpler use cases

Litigation overhang

Appian has been involved in a long running legal dispute with a competitor related to alleged misuse of trade secrets.

This case has:

Produced very large headline verdicts in the past

Been partially overturned and sent back to retrial

Created uncertainty around timing and outcome

Investors should view this as:

Not a core part of the business model

A potential upside surprise or continued overhang

Something that can cause volatility without changing fundamentals

Quarter overview

This earnings report was solid and very on brand. No hype, no blowout headline surprise, but clean execution where it matters most.

The story stayed consistent:

Cloud subscriptions kept growing at a strong clip

Retention stayed healthy

Services grew faster but remained lower margin

Guidance reinforced steady growth rather than acceleration

This was not a “rip your face off” quarter. It was a confidence building quarter.

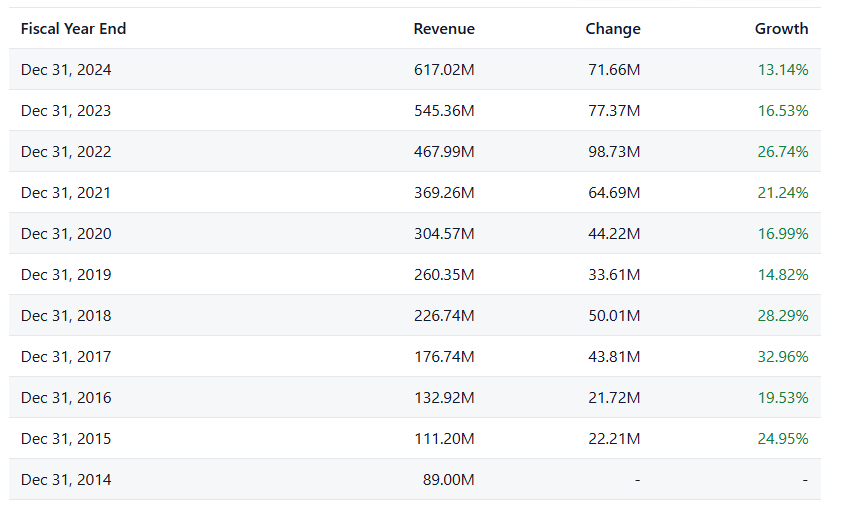

Revenue breakdown

Total revenue

Total revenue grew a little over 20% year over yaer, which keeps Appian firmly in the healthy growth camp for enterprise software tied to large customers and government contracts.

The important part is not just growth, but where it came from.

Cloud subscriptions

This is the metric Wall Street actually cares about.

Cloud subscription reveenue grew low 20s percentt year over year

It made up the majority of total subscription revenue

This line continues to be the primary growth engine

This confirms:

Customers are moving more workloads to Appian’s cloud

Existing customers are expanding usage

The platform remains sticky once deployed

Total subscriptions

Total subscription revenue also grew around 20% year over year, showing that:

Cloud growth is not cannibalizing overall subscription demand

New customer adds plus expansions are both contributing

Professional services

Services revenue grew faster than subscriptions, closer to the high 20s percent range.

This usually happens when:

New deployments ramp

Large projects move from contract to execution

However, management is very clear that services are not the long term margin driver. This growth is supportive but not the main valuation input.

Retention and customer behavior

One of the strongest signals in the report was net revenue retention above 110%.

What that means in plain English:

Customers are not just staying

They are spending more year after year

This tells you:

Appian is not a nice to have tool

Once embedded into workflows, ripping it out is painful

Expansion happens organically as more processes move onto the platform

Retention above 110% is very respectable for enterprise focused software, especially with government exposure.

Customer mix and verticals

Government exposure

Government remained roughly one third of total revenue.

That cuts both ways:

Positive: long contracts, strong security moat, less churn

Negative: lumpy deal timing and budget sensitivity

Importantly, management framed government demand as stable, not weakening.

Commercial enterprise

Commercial customers showed steady demand, particularly in:

Financial services

Insurance

Life sciences

No signs of a collapse in enterprise spending, but also no claim of sudden acceleration. This fits the broader macro environment.

Margins and profitability

Gross margins

Subscription gross margins stayed very high, near the upper 80s percent range

Services margins remained much lower, as expected

This mix dynamic continues to matter. As cloud subscriptions grow faster than services, overall margins should gradually improve.

Operating leverage

Operating losses continued to narrow

Costs were controlled relative to revenue growth

Management is clearly walking the line of:

Grow fast enough to stay relevant

But not burn cash irresponsibly

They are not in a rush to maximize short term profits, but the path toward improved operating leverage is visible.

Cash flow and balance sheet

Cash position remained solid

No liquidity stress signals

No need for near term capital raises

This matters because Appian can:

Invest through slower macro periods

Continue product development

Absorb legal expenses without existential risk

Update Jan15th, 2026

1. Big U.S. Army contract opportunity

Appian announced that the U.S. Army awarded a new Enterprise Agreement that could be worth up to $500 million over 10 years for Appian platform licenses, support, cloud services, and maintenance. The Army also gave conditional Authorization to Operate for Appian Defense Cloud in a secure IL5 environment. This means the Army can deploy Appian’s AI and process automation tech more broadly across its systems.

What it means:

That’s a meaningful commercial validation of Appian’s AI automation platform and a potentially large revenue stream over time. Defense contracts move slower than typical enterprise deals, but this gives Appian a long runway of sales opportunities across the Army’s IT landscape and reinforces its government pipeline